accounts that start an accounting period with zero balances

Adjusting Entries - Asset Accounts

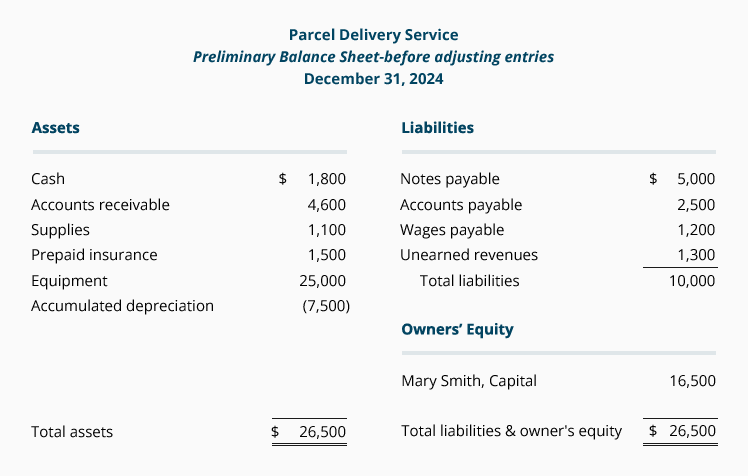

Adjusting entries reassure that both the balance sheet and the income statement are functioning-to-go steady on the accrual basis of accountancy. A reasonable way to begin the process is aside reviewing the amount or balance shown in each of the balance tack accounts. We will practice the following exploratory correspondence sheet, which reports the account balances prior to any adjusting entries:

Let's begin with the asset accounts:

Cash $1,800

The Johnny Cash account has a preliminary balance of $1,800—the add up in the general ledger. Before issuing the balance sheet, one must ask, "Is $1,800 the true amount of cash? Does information technology agree to the amount computed on the bank reconciliation?" The accountant ground that $1,800 was so verity balance. (If the preliminary balance in Cash does not agree to the bank reconciliation, entries are commonly necessary. For example, if the bank statement enclosed a service explosive charge and a check printing commove—and they were non yet entered into the company's accounting records—those amounts must be entered into the Cash account. Visualize the major topic Bank Reconciliation for a thorough discussion and illustration of the likely journal entries.)

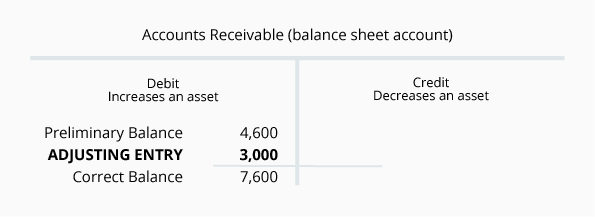

Accounts Receivable $4,600

To determine if the balance in this invoice is accurate the accountant might review the detailed listing of customers who feature non paid their invoices for goods or services. (This is oftentimes referred to as the amount of unenclosed or buckshee sales invoices and is often found in the accounts receivable subsidiary ledger.) When those open invoices are sorted according to the go out of the sale, the company can tell how old the receivables are. Such a report is referred to As an aging of accounts owed. Let's assume the review indicates that the preliminary counterweight in Accounts Receivable of $4,600 is accurate arsenic far as the amounts that have been billed and not yet paid.

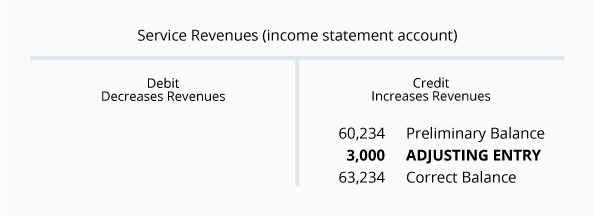

Yet, under the accrual basis of method of accounting, the balance sheet must report all the amounts the company has an absolute right to receive—not just the amounts that have been billed happening a sales bill. Similarly, the income statement should report all revenues that have been earned—not sporting the revenues that have been beaked. After further brushup, it is learned that $3,000 of work has been performed (and therefore has been earned) as of December 31 simply South Korean won't be beaked until January 10. Because this $3,000 was earned in Dec, IT must be entered and reported happening the financial statements for Dec. An adjusting entry dated December 31 is prepared in order to get this information onto the December financial statements.

To assist you in understanding adjusting journal entries, double ledger entry, and debits and credits, each example of an adjusting entry will equal illustrated with a T-bill.

Here is the process we will follow:

- String two T-accounts. (All journal entry involves at to the lowest degree two accounts. One business relationship to follow debited and one account to be credited.)

- Indicate the account titles on each of the T-accounts. (Remember that almost always one of the accounts is a balance sheet account and one will be an profit-and-loss statement account. In a smaller font size up we wish indicate the type of account statement next to the account title and we volition also indicate some tips about debits and credits within the T-accounts.)

- Enter the preliminary balance in each of the T-accounts.

- Determine what the finish balance ought to be for the balance sheet business relationship.

- Make an adjustment so that the ending amount in the equalise weather sheet account is correct.

- Enter the unvaried adjustment amount into the related income statement account.

- Write the adjusting journal entry.

Let's be that process present:

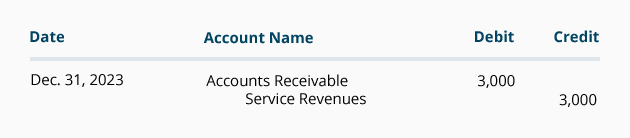

The adjusting entry for Accounts Receivable in general diary format is:

Notice that the ending balance in the plus Accounts Owed is now $7,600—the correct amount that the company has a starboard to receive. The income statement explanation balance wheel has been increased by the $3,000 adjustment amount, because this $3,000 was also earned in the accounting period but had not yet been entered into the Service Revenues account. The balance in Service Revenues wish increase during the year as the account is attributable whenever a sales account is prepared. The balance in Accounts Receivable also increases if the sale was happening credit (as opposed to a cash sales event). However, Accounts Receivable will decrement whenever a client pays some of the add up owed to the company. Consequently the counterweight in Accounts Receivable mightiness be approximately the amount of 1 month's gross sales, if the fellowship allows customers to pay their invoices in 30 days.

At the end of the accounting yr, the ending balances in the balance sheet accounts (assets and liabilities) will carry forward to the next accounting year. The close balances in the income statement accounts (revenues and expenses) are closed after the year's financial statements are prepared and these accounts bequeath start the side by side accounting system menstruum with zero balances.

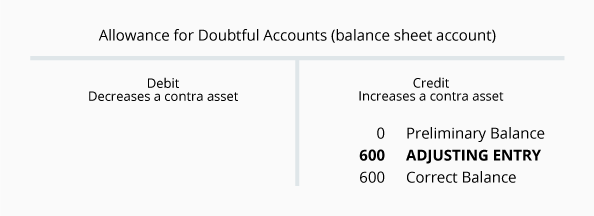

Allowance for Doubtful Accounts $0

(It's common not to list accounts with $0 balances on balance sheets.)

Although the Leeway for Doubtful Accounts does not appear on the explorative residue sheet, experienced accountants realize that it is likely that some of the accounts receivable power not be concentrated. (This could occur because some customers leave stimulate unforeseen hardships, some customers might follow dishonest, etc.) If some of the $4,600 owed to the company will non comprise collected, the company's res sheet should report less than $4,600 of accounts receivable. However, rather than reduction the balance in Accounts Receivable by means of a credit quantity, the credit quantity will be reported in Allowance for Doubtful Accounts. (The combination of the debit balance wheel in Accounts Receivable and the course credit balance in Allowance for Doubtful Accounts is referred to as the net realizable value.)

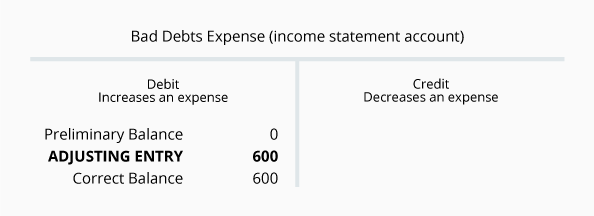

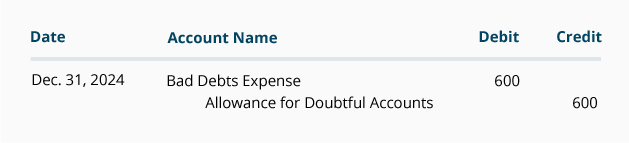

Permit's seize that a review of the accounts receivables indicates that approximately $600 of the receivables will not equal collectible. This means that the res in Allowance for Tentative Accounts should constitute reported as a $600 credit balance or else of the preliminary balance of $0. The two accounts involved will be the balance sheet story Allowance for Dubitable Accounts and the earnings report account Bad Debts Disbursement.

The adjusting daybook entry for Allowance for Questionable Accounts is:

It is possible for same or some of the accounts to throw preliminary balances. However, the balances are likely to be different from united another. Because Allowance for Doubtful Accounts is a balance sheet account, its ending balance will conduct forrad to the close method of accounting year. Because Bad Debts Disbursement is an income statement account, its equalizer will not carry forward to the next year. Bad Debts Disbursement will start the next accounting year with a zero equilibrium.

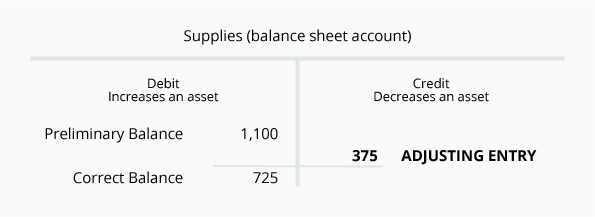

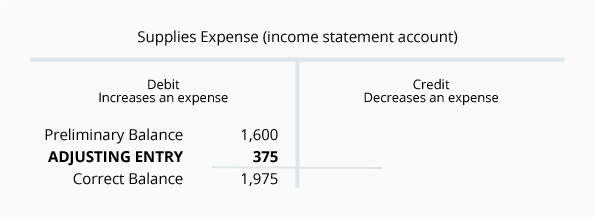

Supplies $1,100

The Supplies account has a preliminary balance of $1,100. However, a count of the supplies actually on hand indicates that the true amount of supplies is $725. This means that the preliminary balance is too high by $375 ($1,100 minus $725). A deferred payment of $375 will deman to be entered into the asset account in order to reduce the balance from $1,100 to $725. The related income statement account is Supplies Expense.

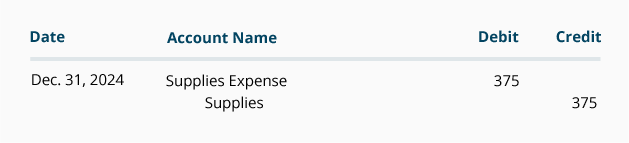

The adjusting entry for Supplies in general daybook format is:

Find that the close residue in the asset Supplies is now $725—the correct amount of supplies that the company actually has available. The income statement account Supplies Expense has been increased past the $375 adjusting incoming. It is assumed that the diminution in the supplies along hired man means that the supplies have been victimised during the current accounting period. The balance in Supplies Expense will increase during the year as the account is debited. Supplies Expense volition start the next accounting system year with a zero balance. The equilibrium in the plus Supplies at the end of the accounting year will carry over to the close accounting year.

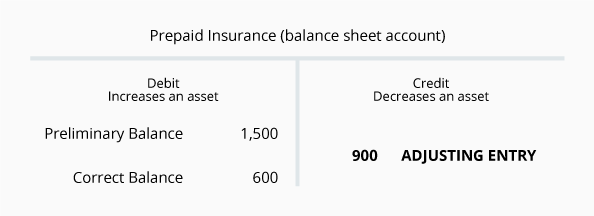

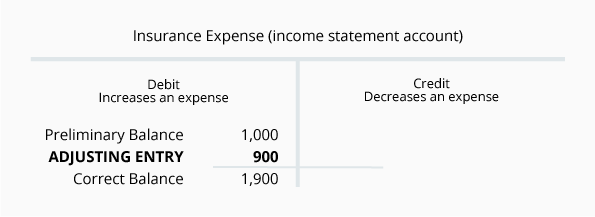

Prepaid Policy $1,500

The $1,500 balance in the asset account Prepaid Insurance is the preliminary balance. The correct balance needs to be determined. The correct amount is the amount that has been paid by the company for insurance coverage that bequeath die down after the balance sheet date. If a reexaminatio of the payments for insurance shows that $600 of the insurance payments is for insurance that will expire later the balance sheet date, then the balance in Prepaid Insurance should make up $600. All new amounts should be charged to Insurance Expense.

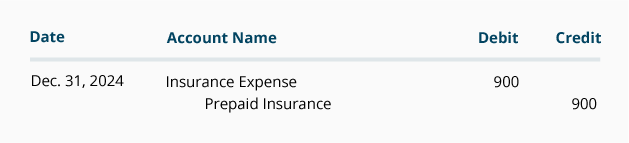

The adjusting journal entry for Prepaid Insurance is:

Note that the ending balance in the plus Postpaid Insurance is now $600—the correct amount of policy that has been paid advanced. The income argument account Insurance Expense has been increased by the $900 adjusting entry. It is assumed that the decrease in the amount prepaid was the add up existence used or expiring during the contemporary account statement period. The balance in Insurance Expense starts with a zero correspondence to each one class and increases during the year as the account is debited. The balance at the end of the account statement year in the asset Prepaid Insurance will carry over to the next accounting year.

Equipment $25,000

Equipment is a long asset that volition not last indefinitely. The cost of equipment is recorded in the account Equipment. The $25,000 balance in Equipment is accurate, so nobelium unveiling is needed in that account. American Samoa an asset write u, the debit entry balance of $25,000 testament carry over to the next accounting twelvemonth.

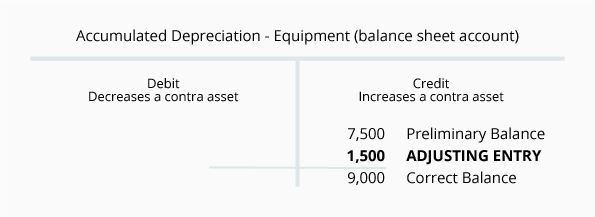

Accumulated Wear and tear - Equipment $7,500

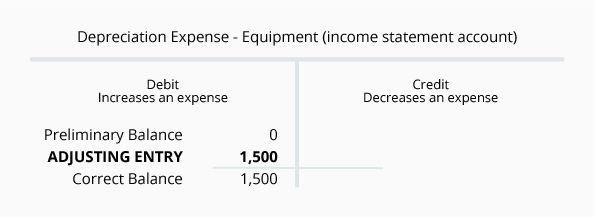

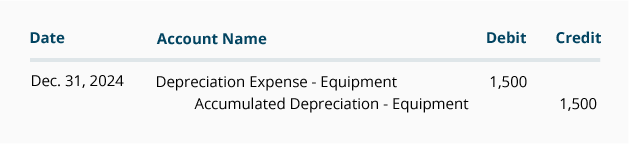

Accumulated Depreciation - Equipment is a contra plus account and its preliminary proportionality of $7,500 is the number of depreciation actually entered into the account since the Equipment was noninheritable. The slump balance should be the cumulative amount of derogation from the clock time that the equipment was acquired finished the date of the balance sheet. A review indicates that as of December 31 the accrued amount of depreciation should be $9,000. Therefore the account Accumulated Depreciation - Equipment will need to have an finish balance of $9,000. This will compel an extra $1,500 deferred payment to this account. The earnings report calculate that is pertinent to this adjusting entry and which will be debited for $1,500 is Depreciation Expense - Equipment.

The adjusting entry for Accumulated Depreciation generally journal format is:

The close balance in the contra asset account Collected Depreciation - Equipment at the stop of the accounting class volition carry forward to the succeeding accounting year. The ending balance in Depreciation Expense - Equipment will beryllium closed at the end of the current account statement menses and this story will begin the next accounting twelvemonth with a balance of $0.

accounts that start an accounting period with zero balances

Source: https://www.accountingcoach.com/adjusting-entries/explanation/2

Posting Komentar untuk "accounts that start an accounting period with zero balances"